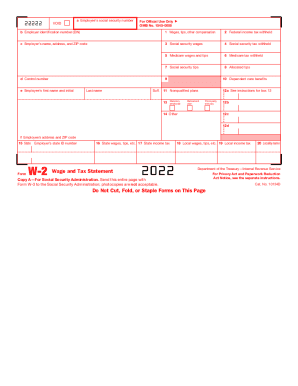

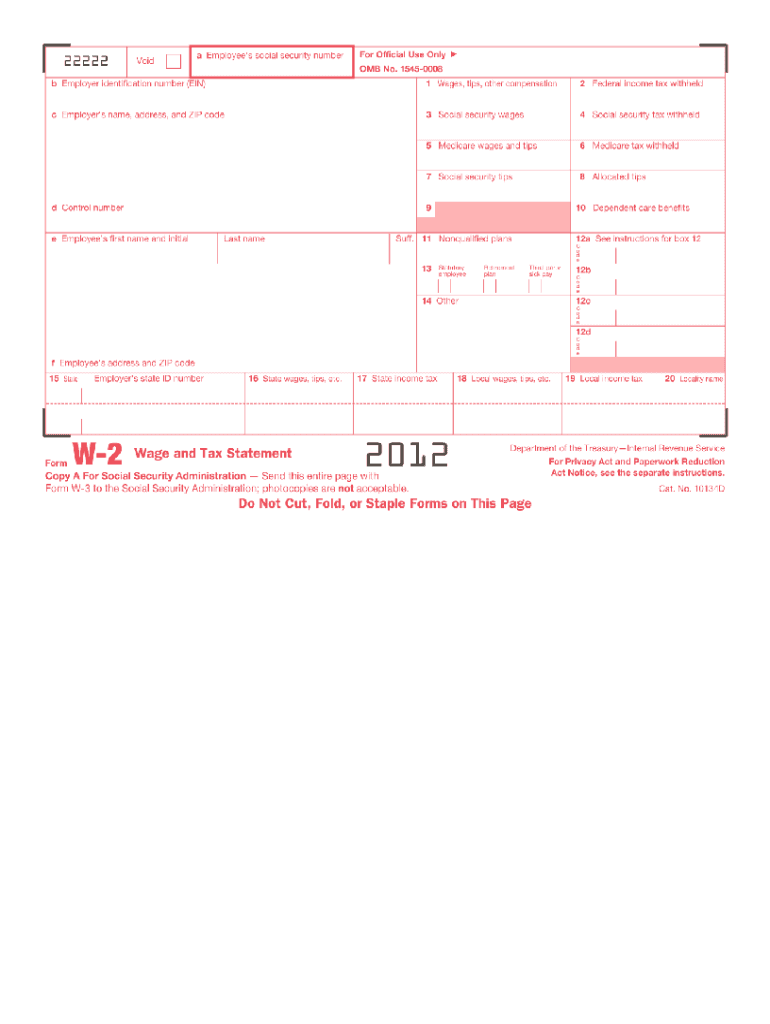

Form W-2, Wage and Tax Statement

Who files Form W-2?

Any employer must file Form(s) W-2 if it has one or more employees to whom it made payments (including noncash payments) for the employees’ services in the trade or business of the employer during 2017.

The employer completes and files Form W-2 for each employee for whom any of the following applies (even if the employee is related to the employer).

-

The employer withheld any income, social security, or Medicare tax from wages regardless of the amount of wages; or

-

The employer would have had to withhold income tax if the employee had claimed no more than one withholding allowance or had not claimed exemption from withholding on Form W-4; or

-

The employer paid $600 or more in wages even if you did not withhold any income, social security, or Medicare tax.

Only in very limited situations the employer will not have to file Form W-2. This may occur if the employer were not required to withhold any income tax, social security tax, or Medicare tax and the employer paid the employee less than $600, such as for certain election workers and certain foreign agricultural workers.

When is Form W-2 due?

Mail or electronically file Copy A of Form(s) W-2 with the Social Security Administration by January 31, 2018. You may owe a penalty for each Form W-2 that you file late.

How do I fill out Form W-2?

Box 1. Enter the amount of wages, tips, other compensation.

Box 2. Enter the amount of the federal income tax withheld.

Box 5. You may be required to report this amount on Form 8959, Additional Medicare Tax. See the Form 1040 instructions to determine if you are required to complete Form 8959.

Box 6. This amount includes the 1.45% Medicare Tax withheld on all Medicare wages and tips shown in box 5, as well as the 0.9% Additional Medicare Tax on any of those Medicare wages and tips above $200,000.

Box 8. This amount is not included in boxes 1, 3, 5, or 7. For information on how to report tips on your tax return, see your Form 1040 instructions. You must file Form 4137, Social Security and Medicare Tax on Unreported Tip Income, with your income tax return to report at least the allocated tip amount unless you can prove that you received a smaller amount. If you have

records that show the actual amount of tips you received, report that amount even if it is more or less than the allocated tips. On Form 4137 you will calculate the social security and Medicare tax owed on the allocated tips shown on your Form(s) W-2 that you must report as income and on other tips you did not report to your employer. By filing Form 4137, your social security tips will be credited to your social security record (used to figure your benefits).

Box 10. This amount includes the total dependent care benefits that your employer paid to you or incurred on your behalf (including amounts from a section 125 (cafeteria) plan). Any amount over $5,000 is also included in box 1. Complete Form 2441, Child and Dependent Care Expenses, to compute any taxable and nontaxable amounts.

Box 11. This amount is (a) reported in box 1 if it is a distribution made to you from a nonqualified deferred compensation or nongovernmental section 457(b) plan or (b) included in box 3 and/or 5 if it is a prior year deferral under a nonqualified or section 457(b) plan that became taxable for social security and Medicare taxes this year because there is no longer a substantial risk of forfeiture of your right to the deferred amount. This box should not be used if you had a deferral and a distribution in the same calendar year. If you made a deferral and received a distribution in the same calendar year, and you are or will be age 62 by the end of the calendar year, your employer should file Form SSA-131, Employer Report of Special Wage Payments, with the Social Security Administration and give you a copy.

Box 12. The following list explains the codes shown in box 12. You may need this information to complete your tax return. Elective deferrals (codes D, E, F, and S) and designated Roth contributions (codes AA, BB, and EE) under all plans are generally limited to a total of $18,000 ($12,500 if you only have SIMPLE plans; $21,000 for section 403(b) plans if you qualify for the

15-year rule explained in Pub. 571). Deferrals under code G are limited to $18,000. Deferrals under code H are limited to $7,000.

Where do I send Form W-2?

Form W-2 is a multi-part form. Send Copy A to the SSA; Copy 1, if required, to your state, city, or local tax department; and Copies B, C, and 2 to your employee. Keep Copy D with your records for 4 years.